An Open Letter About the Budget Proposal to Tax Testamentary Discretionary Trust Income at 30%

If you would like to download a version of this letter to add to your own letterhead and send to your Member of Parliament, you can download it here:

Download NowExecutive Summary

- This submission concerns the Federal Budget 2026-2027 announcement that the Government intends to introduce a 30% minimum tax on discretionary trusts from 1 July 2028, with the trustee paying tax and beneficiaries, other than corporate beneficiaries, receiving non-refundable credits for tax paid by the trustee.

- My concern is that testamentary discretionary trusts are being caught up in a broader policy conversation about discretionary trusts, income splitting and tax minimisation, without sufficient recognition of their unique role in estate planning.

- The primary purpose of testamentary discretionary trusts is to protect an inheritance for children, widows, widowers, disabled beneficiaries and vulnerable adults after a person’s death.

- I respectfully submit that testamentary discretionary trusts should either be excluded from the proposed minimum tax regime entirely, or at the very least, the existing adult marginal tax rates should be preserved for income distributions to minors, disabled beneficiaries and low income beneficiaries.

- The key facts are:

(a) a testamentary discretionary trust can only arise because somebody has died. It is not possible to create a testamentary discretionary trust in circumstances other than a person’s death;

(b) the only assets which can be owned by a testamentary discretionary trust under the current tax position are the assets which the willmaker owned at the date of their death i.e. inheritance assets. The existing tax regime heavily disincentivises the injection of non inheritance assets into a testamentary discretionary trust;

(c) there are less than 11,000 active testamentary discretionary trusts currently in existence in Australia (compared to over 840,000 discretionary trusts) - this is not a widespread tax integrity problem;

(d) the main driver for utilising a testamentary discretionary trust compared to a standard will is protection - protecting the inheritance for children, widows, widowers, disabled beneficiaries, and vulnerable adults after death; and

(e) under the proposed new minimum 30% tax regime:

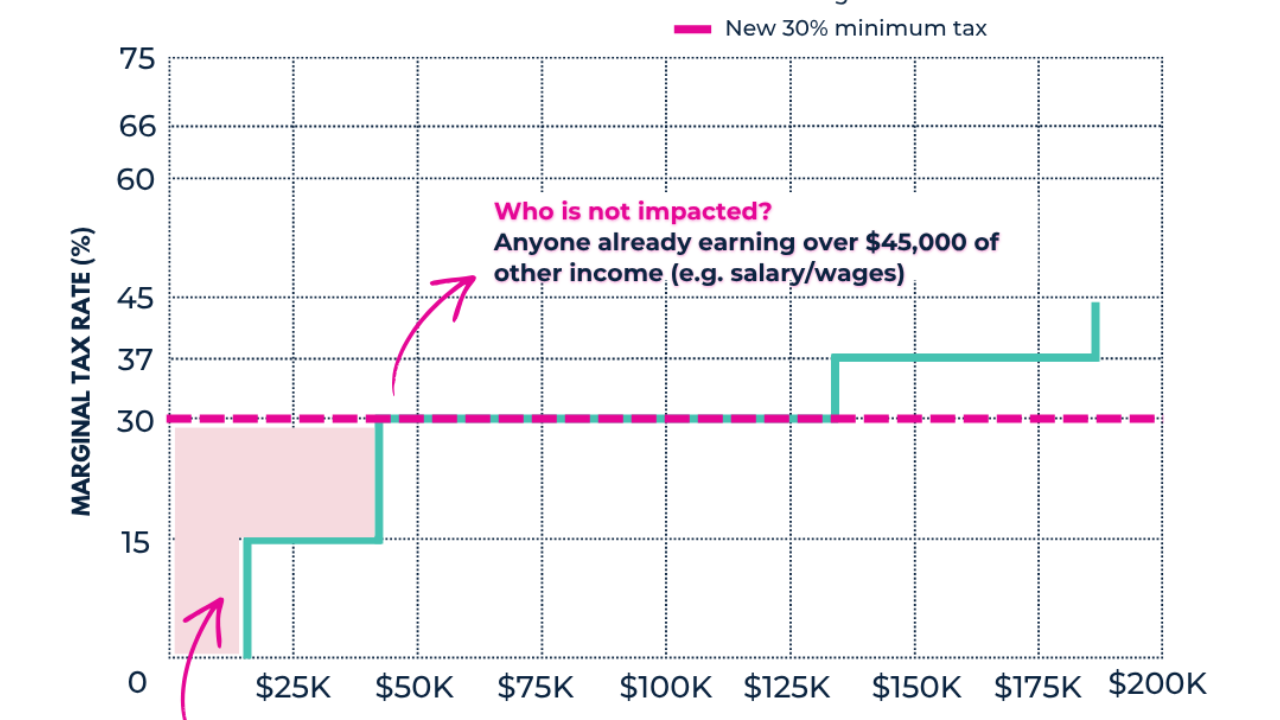

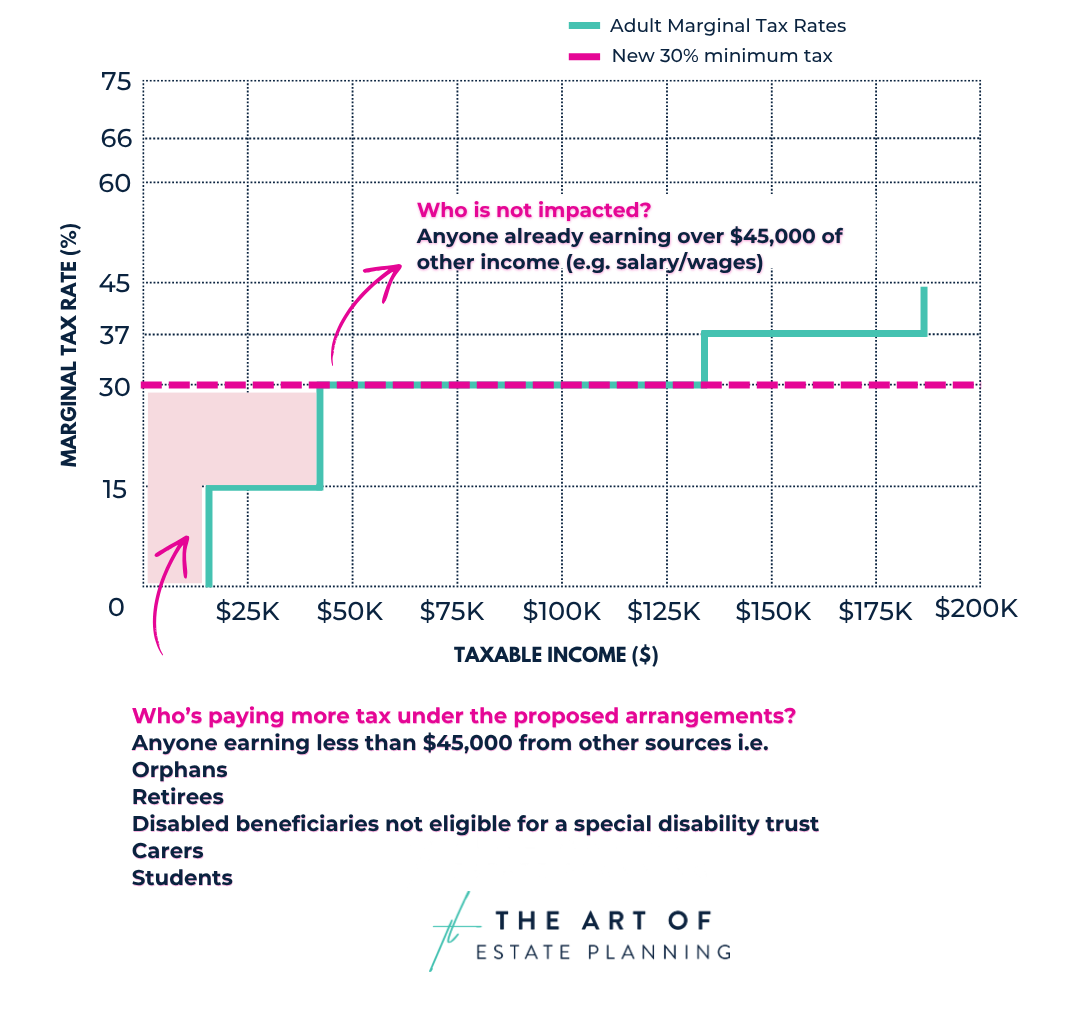

(i) an adult who is earning at least $45,000 of income from sources other than trust distributions (e.g. salary, wages, directly held investments) will already pay a minimum of 30% tax on trust distributions, resulting in no additional tax paid under the new tax regime;

(ii) however, beneficiaries who earn less than $45,000 of income from sources other than trust distributions will lose access to the tax free threshold and 14% marginal tax rate (which is expected to be in effect by 1 July 2028 when these measures take effect) on the income from their inheritance; and

(iii) single and double orphans, minors raised by grandparents, retirees, disabled beneficiaries who do not qualify for a special disability trust, adults in the ‘sandwich generation’ who have reduced their employment in order to caring for aging parents and children/grandchildren, and adult students will be penalised by the new regime, with no impact on high income earners.

What is a Testamentary Discretionary Trust?

-

A testamentary discretionary trust, often called a TDT, is a discretionary trust created by a person’s will. It does not exist during the willmaker’s lifetime. It only comes into existence after the willmaker has died.

-

This is very different from an ordinary discretionary family trust established during life

-

A testamentary discretionary trust is commonly used to:

-

protect young adults and minor children from receiving control of substantial inheritances too early and exposing the inheritance to the influence of bad actors, financial exploitation and financial immaturity;

-

preserve an inheritance for the benefit of a willmaker’s children, so that the inheritance is not exposed to risks where a surviving spouse re-partners and then subsequently dies or experiences a relationship breakdown;

-

protect an inheritance for the benefit of a willmaker’s lineal descendants and prevent it from being exposed to a beneficiary’s bankruptcy risks if that beneficiary is a director of a business, operating as a sole trader or in a high-risk occupation;

-

provide flexible support for disabled or vulnerable beneficiaries (noting the longstanding legal principle that minors are inherently vulnerable purely because of their age and cannot contract or hold assets); and

-

give a surviving spouse tax flexibility about how the inheritance and the income it generates can be allocated between themselves and the needs of their children, without divesting themselves of their inheritance.

-

Current Treatment of Testamentary Discretionary Trusts

-

The current tax treatment of testamentary trusts reflects the longstanding distinction between testamentary discretionary trusts and family trusts.

-

Any income in excess of $416 from a family trust distributed to a minor will be taxed at penalty marginal rates (i.e. 66% for income between $417 -$1,307, and 45% for income in excess of $1,308).

-

Income distributed to minors from a testamentary discretionary trust is taxed at the standard adult marginal tax rates. This longstanding treatment recognises that the income has been generated from investment of an inheritance.

-

In particular, distributions to minors from a family trust is artificial income splitting.

-

Distributions to minors from a testamentary discretionary trust are as a result of the child receiving support from an inheritance.

-

The Budget announcement indicates that existing testamentary discretionary trusts will be excluded from the proposed regime. If existing Testamentary discretionary trusts deserve protection because they are testamentary, future testamentary discretionary trusts deserve proper consideration for the same reason. No family creates a testamentary discretionary trust unless someone has died. A child whose parent dies in 2029 is no less vulnerable than a child whose parent died in 2025.

Reasons for using a Testamentary Discretionary Trust

-

Much of the public commentary about these proposed changes has focused on tax.

-

However, in estate planning practice, the tax concessions are only one small part of the reason families use testamentary discretionary trusts and in many cases, tax is not the primary driver at all.

-

The non-tax benefits of testamentary discretionary trusts include:

-

protection of the willmaker’s children from losing an inheritance to a step-parent or new family unit where a surviving spouse re-partners and later dies or experiences a relationship breakdown;

-

protection of an inheritance for a willmaker’s grandchildren where an adult child experiences a relationship breakdown, or experiences bankruptcy;

-

protection for disabled or vulnerable beneficiaries;

-

protection of young adults from receiving control of substantial inheritances too early;

-

flexibility to share an inheritance amongst a family unit to adapt to future illness, disability or hardship; and

-

long-term succession planning across generations.

-

-

Families are more complex than they were in previous generations. Blended families are common. Relationship breakdown is common. Adult children are often financially stretched. Housing affordability is a major issue. Many people are starting businesses or acting as company directors, which creates financial risk.

-

Inheritance is one of the few ways many younger Australians may be able to get ahead.

-

Willmakers will continue to use testamentary discretionary trusts in their wills after the proposed commencement date of 1 July 2028. However, they will now be asked to pay a tax penalty for this protection. The proposed regime primarily impacts lower income families because beneficiaries already earning more than $45,000 are generally paying tax at or above 30%.

-

The table below sets out specific case studies highlighting the advantages of a testamentary discretionary trust for different demographics:

| Basic Will | Testamentary Discretionary Trust Will | |

|---|---|---|

| Double Orphan Minor Child | • Child can demand money when they turn 18 (even if the will says it is held on trust until they turn a specific age e.g. 25), exposing the inheritance to their financial immaturity • No asset protection benefits from relationship breakdown or bankruptcy risks once the child reaches adulthood • Depending on the terms of the will, there may be limited flexibility to deal with inheritance funds until the child reaches 18 |

• Child cannot demand the inheritance when they turn 18 – they can benefit from the inheritance whilst still a minor and once they turn 18 but the inheritance is not exposed to their financial immaturity • Child can take over control of the trust at an appropriate age once they are financially responsible • Inheritance has increased protection from relationship breakdown and bankruptcy risks once child reaches adulthood |

| Surviving Spouse and Single Orphan Minor Children Ava dies. Her husband Dan and their three minor children survive her |

• If Dan re-partners, the inheritance is automatically exposed to family law proceedings if he separates from his new spouse • Ava’s children are relying on Dan’s new will to gift the remainder of the inheritance to them, exposing them to the risk that Dan’s will leaves his assets (including the inheritance from Ava) to his new spouse or Dan contributes the inheritance towards assets owned jointly with a new spouse which are excluded from his will • The inheritance is exposed to family provision application risks from Dan’s new spouse, any new children upon Dan’s death • If Dan is running a business or in a high-risk occupation, the inheritance is exposed to claims from creditors |

• The inheritance from Ava is not automatically part of the property pool in family law proceedings if Dan re-partners and experiences a relationship breakdown • Ava has already set up the succession plan through the trust to pass her inheritance ultimately to her kids on Dan’s death, and is not relying on Dan’s new will • The inheritance is insulated from a family provision application against Dan's estate (except in New South Wales) • The inheritance is protected from claims by Dan’s creditors |

| Minor Raised by Grandparents Sarah is a minor and raised by her grandparents. Her parents are still alive but are estranged from the family, suffering from substance abuse and mental health issues |

• Sarah can demand money when she turns 18 (even if the will says it is held on trust until they turn a specific age e.g. 25), exposing the inheritance to their financial immaturity and influence of bad actors (e.g. her parents) • No asset protection benefits from relationship breakdown or bankruptcy risks once Sarah reaches adulthood • Depending on the terms of the will, there may be limited flexibility to deal with inheritance funds until Sarah reaches 18 |

• Sarah cannot demand the inheritance when she turns 18 – she can benefit from the inheritance whilst still a minor and once she turns 18 but the inheritance is not exposed to their financial immaturity. Sarah’s grandparents can choose trusted family members or friends to take financial responsibility for the inheritance and manage it for Sarah’s benefit until Sarah is financially mature • Sarah can take over control of the trust at an appropriate age once she is financially responsible • Inheritance has increased protection from relationship breakdown and bankruptcy risks once Sarah reaches adulthood |

| Adult Child Josh, who is married to Louise and together they have 2 minor children |

• The inheritance is automatically part of the property pool in family law proceedings if Josh experiences a relationship breakdown • There’s a high likelihood that Josh’s will leaves everything to Louise. If Josh later dies and then Louise re-partners, there’s no certainty that the inheritance will be received by Josh’s children, as Louise’s new will could leave the inheritance to a new spouse or future children • If Josh is running a business or in a high-risk occupation, the inheritance is exposed to claims from creditors |

• The inheritance is not automatically part of the property pool in family law proceedings if Josh experiences a relationship breakdown • If the inheritance is received via a testamentary trust for Josh and his children, then Josh’s will (and therefore Louise's will) is irrelevant in relation to the inheritance and the willmakers have comfort their grandchildren will benefit from any remaining inheritance • The inheritance stays in the testamentary discretionary trust for the benefit of Josh’s children after Josh dies, and can be managed for his children by trusted friends/family members • The inheritance is protected from claims by Josh’s creditors |

Tax Consequences for Young Families Who Lose a Parent – Surviving Spouses and Single Orphans

- One of the most concerning consequences of the proposed changes is the potential impact on young families where one parent dies.

- While we understand that the exemption for income distributions from a testamentary discretionary trust to ‘vulnerable minors’ mentioned in the Budget material would include double orphans, this exemption should also be extended to include all minors.

- Where a parent dies leaving a surviving spouse and young children, a testamentary discretionary trust can allow income generated from the inheritance to be used tax effectively for the children.

- This can make a meaningful difference for a young family who has lost a breadwinner, where the widow/widower is trying to financially support the family whilst grieving.

- The current ability to allocate part of the income generated from an inheritance to the minor children tax effectively recognises that the surviving spouse will often have to incur additional expenses to fund family support, for instance, childcare, cleaning, housekeeping, meal preparation, transport, and yard maintenance services etc.

- This would not affect wealthy tax planners only, but everyday Australian families struggling to make ends meet in a cost of living crisis.

Diverse family structures

- The existing taxation treatment of testamentary discretionary trusts which allows all minors to be taxed at adult marginal tax rates affords flexibility to recognise that families don’t always fit traditional structures.

- Consider:

- grandparents who are raising their grandchildren because the parents are not willing to or capable of raising their children; and

- children who still have one parent still living but that surviving parent is estranged, incapacitated or unwilling to act as their parent.

- grandparents who are raising their grandchildren because the parents are not willing to or capable of raising their children; and

Fixed Testamentary Trusts Are Not an Equivalent Alternative

- The Budget material suggests that fixed testamentary trusts will be excluded from the 30% income tax regime.

- However, fixed testamentary trusts are not an adequate substitute for testamentary discretionary trusts.

- A fixed testamentary trust does not offer any of the protection benefits provided by testamentary discretionary trusts. In practice, fixed testamentary trusts are unsuitable for many families seeking the flexibility and protection benefits of a testamentary discretionary trust.

| Basic Will | Fixed Testamentary Trust | Testamentary Discretionary Trust | |

|---|---|---|---|

| Family Law and Bankruptcy Protection | No | No | Yes |

| Tax treatment of income distributions to adults | Marginal Tax Rates | Marginal Tax Rates | Minimum 30% and then marginal tax rates |

| Multi-generational succession planning | No | No | Yes |

| Protecting financially immature beneficiaries | No | No | Yes |

| Ability to control your own inheritance | No | No (the beneficiary cannot be the trustee) | Yes |

- Further, the existing definition of a fixed trust in the tax legislation is very confusing and difficult to satisfy (being housed in the division of the legislation dealing with Trust Losses), with many taxpayers needing to apply for the Commissioner’s specific discretion to determine whether a trust is a fixed trust, or rely on safe harbour provisions set out in Practice Compliance Guidelines 2016/16. This uncertainty and complexity further adds to the confusion about how to create a fixed testamentary trust will that satisfies the exemption.

Transitional complications

- There is current uncertainty about whether the exemption for existing testamentary discretionary trusts will apply to testamentary discretionary trusts where the willmaker died before 12 May 2026, but the trust has not yet been established as the estate is still being administered (which can typically take between 12 months and 3 years).

- This uncertainty will add to the delay in finalising the estate administration and leave families in limbo while they wait for clarity from the Government.

- At a minimum, grandfathering should apply to:

- all testamentary discretionary trusts established by a will where the willmaker has died on or before 12 May 2026, irrespective of when the estate assets are distributed to the testamentary trust; and

- all wills signed before 1 July 2028, even if the willmaker has not yet died.

- all testamentary discretionary trusts established by a will where the willmaker has died on or before 12 May 2026, irrespective of when the estate assets are distributed to the testamentary trust; and

Specific Recommendations

- I respectfully submit that the Government should exclude testamentary discretionary trusts from the proposed 30% minimum tax regime entirely.

- This recognises that testamentary discretionary trusts are fundamentally different from standard discretionary trusts and preserves the longstanding policy distinction between artificial income splitting and post-death family protection. It also ensures that beneficiaries who are orphan children, disabled and vulnerable adult beneficiaries or low income earners are not penalised for accessing the protection they require.

- If all testamentary discretionary trusts are not excluded from the proposed 30% tax regime, then:

- the 30% minimum tax should not apply to minors, disabled beneficiaries and charities;

- existing wills signed before 1 July 2028 should be grandfathered and excluded;

- testamentary discretionary trusts established by the will of a person who has died before 12 May 2026 should be excluded, irrespective of whether the testamentary discretionary trust has been established;

- the Income Tax legislation should include a clear definition of vulnerable beneficiaries which does not require exercise of the Commissioner’s discretion;

- the Income Tax legislation should be amended to introduce a clear definition of fixed trusts; and

- further consultation should occur with estate planning lawyers, tax advisers, accountants, disability advocates, family law practitioners and community organisations before legislation is introduced.

- the 30% minimum tax should not apply to minors, disabled beneficiaries and charities;

- If you have any questions or require clarification on any aspect, I would be more than happy to assist.

Yours sincerely,

Tara Lucke

Lawyer and Director, The Art of Estate Planning Pty

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.